Keywords: Digital Currency

-

AUSTRALIA

- Mark Gaetani

- 26 February 2025

As cash fades from everyday transactions, its decline underscores a growing divide in access. With digital payments dominating and cash use dropping sharply, questions loom over the future of currency in an increasingly cashless society, and who might be left behind.

READ MORE

-

AUSTRALIA

- Binoy Kampmark

- 04 February 2025

Smartphones dictate access to commerce, communication, and even education, and face-to-face transactions have all but disappeared. Have we willingly surrendered choice for convenience? As digital payments become the norm, are those choosing to live without a smartphone excluded from modern society?

READ MORE

-

INTERNATIONAL

- David Halliday

- 19 August 2024

1 Comment

After a year in court, a U.S. Judge concluded that Google has a monopoly over search and had illegally maintained its monopoly by making massive payments to other companies to be their default search engine. Everyone in tech is quietly watching for what happens next, because how the U.S. Department of Justice treats Google will set the example for the other giants standing astride the world.

READ MORE

-

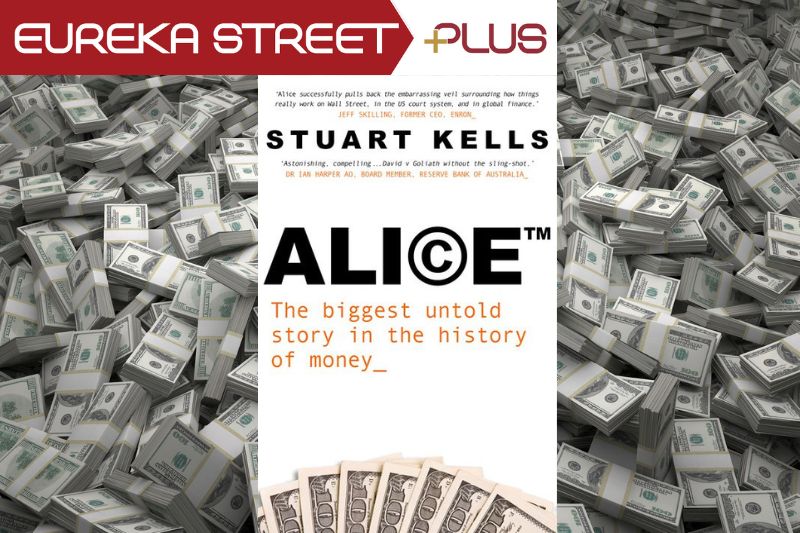

ECONOMICS

It is a truism to say that the way money is constructed defines the power structure under which we live. But allowing private actors to manipulate and game the financial system has not just given them extraordinary power, it has undermined the way money itself is understood.

READ MORE

-

INTERNATIONAL

- Max Jeganathan

- 21 November 2023

1 Comment

The spectacular rise and fall of Sam Bankman-Fried is a story that began with unfettered brilliance and financial wizardry, but quickly unraveled into an all-too familiar cautionary tale of swindlers, conmen, and morally vacuous ambition.

READ MORE

-

ECONOMICS

Monetary authorities are caught in an impossible situation. Inflation is rising: it is over 5 per cent in Australia and over 9 per cent in the United States. Inflation is often seen as a way out of excessive debt because it erodes the real value of money and therefore the real value of the debt. But what is increasingly being discussed are ways to cancel the debt.

READ MORE